In 2008, while the financial world was collapsing and people were losing half their retirement savings overnight, Ray Dalio—the billionaire founder of the world’s largest hedge fund—was fielding panicked calls from friends and family.

During this time, everyone wanted to know the same thing: “What do I do with my money?”

Dalio had spent decades studying economic history, analyzing how markets behaved during the Great Depression, the stagflation of the 1970s, the tech bubble, and countless other crises.

In fact, he even documented what he learned and found here in this video:

Over his decades studying the economy and investing, Dalio noticed a pattern: investors kept getting destroyed because they bet everything on one economic “season.” When that season changed, their portfolios got wrecked.

So he designed something different. Something that could weather any storm.

Years later, when Tony Robbins was researching his book Money: Master the Game, he asked Dalio a simple question: “If you couldn’t pass wealth to your family but could only give them a set of investment principles, what would it be?”

Dalio’s answer became known as the “All Seasons” portfolio—and it’s one of the most powerful tools you’ve probably never heard of.

The Four Seasons of Money

Here’s the thing most of us get wrong about investing: we think the goal is to pick the winners. Find the hot stock. Time the market. Beat everyone else.

But Dalio realized something more fundamental. The economy moves through four seasons, and most portfolios are dressed for only one:

- Rising growth (the good times—stocks soar)

- Falling growth (recession—stocks tank)

- Rising inflation (your money loses buying power)

- Falling inflation (deflation—cash is king)

Think about your current investments. If you’re like most people, you’re probably heavy in stocks, maybe some bonds. You’re dressed for summer, but what happens when winter comes?

The All Seasons portfolio is like packing clothes for every type of weather before a trip where you don’t know the forecast. It’s built to survive—and even thrive—no matter what economic season we’re in.

Breaking Down the All Seasons Strategy

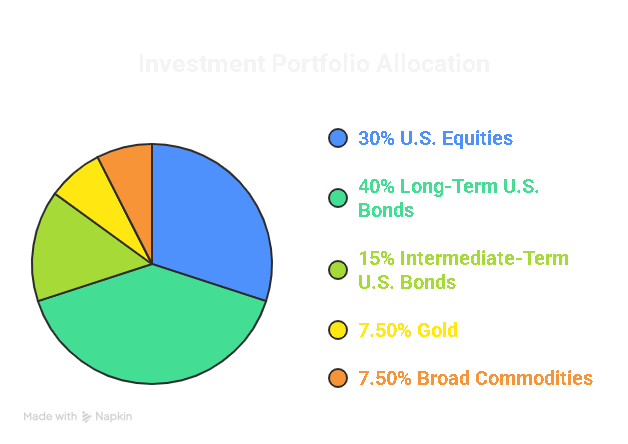

Here’s the actual allocation Dalio shared:

- 30% in stocks (U.S. equities)

- 40% in long-term U.S. bonds (long-term Treasuries)

- 15% in intermediate-term U.S. bonds (intermediate Treasuries)

- 7.5% in gold

- 7.5% in broad commodities (not including gold)

This is how it would look:

Let’s look at an example. Say you’ve finally hit that first major milestone—$100,000 saved (which BTW, that’s AMAZING!)

Instead of putting it all in a single index fund and praying the market keeps going up, you’d split it like this:

- $30,000 in a broad stock index fund (30%)

- $40,000 in a long-term Treasury fund (40%)

- $15,000 in an intermediate Treasury fund (15%)

- $7,500 in a gold fund (7.5%)

- $7,500 in a diversified commodities fund (7.5%)

Then, once a year, you rebalance back to these percentages. That’s it. No market timing. No panic selling. No CNBC-induced anxiety.

Think of it like a thermostat for your money. When one asset class runs hot, you sell a bit and buy what’s gotten cold. You’re automatically buying low and selling high without trying to outsmart the market.

But Why So Much in Bonds?

I know what you’re thinking. “Wait—55% in bonds? That sounds boring. That sounds like something my grandparents would do. I’m young. I should be aggressive!”

Hey, as someone who put his whole retirement bonds early on, and missed out on thousands of dollars of compound growth…I understand.

That little voice is the naysayer in all of us talking.

But here’s the counterintuitive truth: this portfolio isn’t designed to make you rich quickly. It’s designed to keep you in the game during the times that destroy everyone else.

This portfolio strategy is designed to minimize risk and maximize upside.

During the 2008 financial crisis, a traditional 60/40 stock-bond portfolio lost about 20-30%. People panicked, sold at the bottom, and they never recovered emotionally, even if they eventually recovered financially.

Here’s the crazy part: Ray Dalio’s All Seasons approach that I’m sharing with you barely flinched.

It went down only about 3-4%.

And that emotional stability is worth more than any potential upside you’re chasing.

Because the real enemy isn’t missing out on gains. It’s getting knocked out of the game entirely when disaster strikes.

Remember: you come from a background where there’s no safety net. You don’t have generational wealth to fall back on. You can’t afford to lose half your portfolio and shrug it off. This strategy understands that your risk isn’t just financial—it’s existential.

The Engineer’s Advantage

Here’s where this gets interesting for you specifically.

As engineers, you’re trained to think in systems. You understand redundancy. You know that the best designs aren’t the flashiest—they’re the ones that don’t fail. A bridge isn’t impressive because it looks good on a sunny day; it’s impressive because it stands strong during the earthquake.

The All Seasons portfolio is the engineering approach to investing. It’s not about optimization for perfect conditions. It’s about robustness across all conditions.

You already know how to build things that last. Now apply that same principle to your money.

And here’s the beautiful part: you don’t need to be rich to start. You can build this with $5,000, $10,000, or $50,000. The percentages stay the same. Most brokerages now offer fractional shares and low-cost ETFs that make this accessible to anyone.

Ask Yourself

Before you do anything else, sit with these questions:

- What economic season is your current portfolio dressed for? If you’re 100% in stocks, you’re betting everything on rising growth. What happens when that season ends?

- How would you feel if your portfolio dropped 30% tomorrow? Not intellectually—emotionally. Would you panic? Sell? If the honest answer is yes, your risk is too high.

- Are you investing based on principles, or based on what everyone else is doing? Following the crowd feels safe until the crowd runs off a cliff together.

- What does financial freedom actually mean to you? Is it a number? A feeling? The ability to weather any storm without fear? Provide for your family and have work as an option?

Thinking Ahead…

This approach is simple. It’s not meant to give you the HIGHEST returns period…but it’s meant to give you the highest returns with the lowest downside.

Even better, it will help you have sleep, stability, and the confidence that comes from knowing your financial foundation can’t be shaken by a single bad headline or economic downturn.

You’re already beating the odds by being here, by saving, by thinking about this stuff. You’ve worked too hard to build what you have to risk it on a strategy that only works during good times.

I’m here with you in the trenches. I will build my personal All Seasons portfolio step by step, little by little, deposit by deposit.

Because the goal isn’t just to make money—it’s to keep it, grow it steadily, and never have to start over.

Alex